July 8, 2025

Learn sales, ops, and leadership skills to grow your mortgage career and team success.

Mar 28, 2025

Explore assumable mortgage loans and what this means for buyers and sellers.

March 1, 2025

Explore the in's and out's of becoming a mortgage loan officer.

Jan 3, 2025

Keep your MLO license active with fresh, engaging, and state-specific NMLS Late CE training.

Jan 2, 2025

A short look at NMLS Late CE for MLOs who missed their annual CE deadline.

Oct 3, 2024

Here's what every loan officer should know about RESPA to stay compliant.

July 29, 2025

Strong leaders steady the ship. Explore 7 traits that set great mortgage leaders apart.

Apr 28, 2025

UWM’s “All-In” contract faces legal scrutiny. See what’s happening in this antitrust lawsuit.

Get the full scoop on Freddie Mac's changes to ADU rules.

March 28, 2025

When you hit a rut in your career, the way out may not be the easiest but it could be the most rewarding.

Feb 6, 2025

CFPB changes bring along a wave of changes. Here’s what mortgage professionals need to know.

Oct 22, 2024

AI is reshaping mortgages. Learn how to prepare your business for the future.

September 8, 2025

Master social media with Michelle Berman-Mikel’s Beyond the Method™, now on Coop+.

August 20, 2025

Learn how to upload and organize documents into Coop AI Custom Collections.

July 30, 2025

Knowledge Coop's step-by-step guide to using Coop AI Custom Collections.

July 17, 2025

Knowledge Coop welcomes a new CEO, marking a bold new chapter in the company.

June 26, 2025

Boost mortgage leadership skills with a new masterclass series built with Building Champions.

June 23, 2025

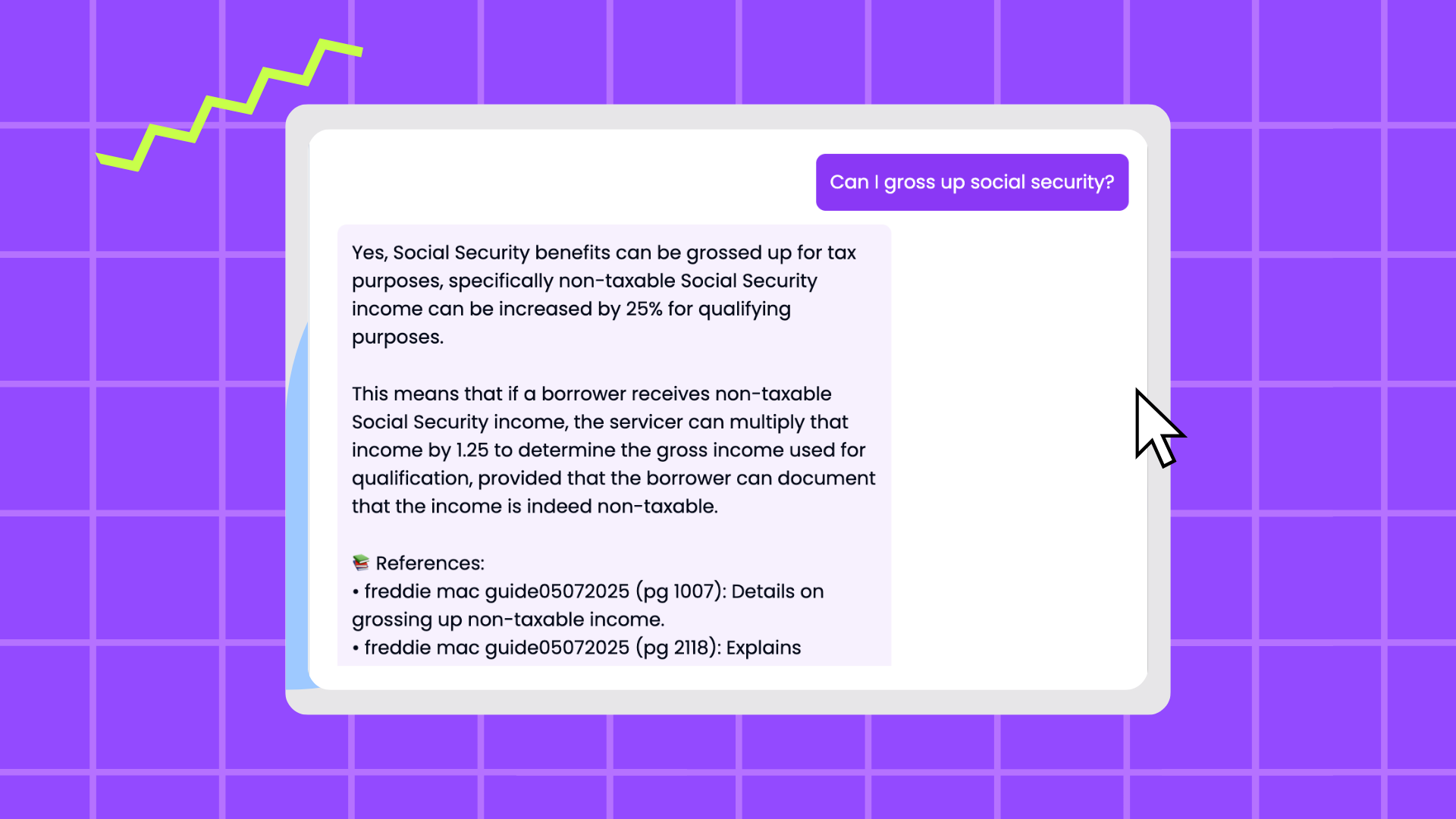

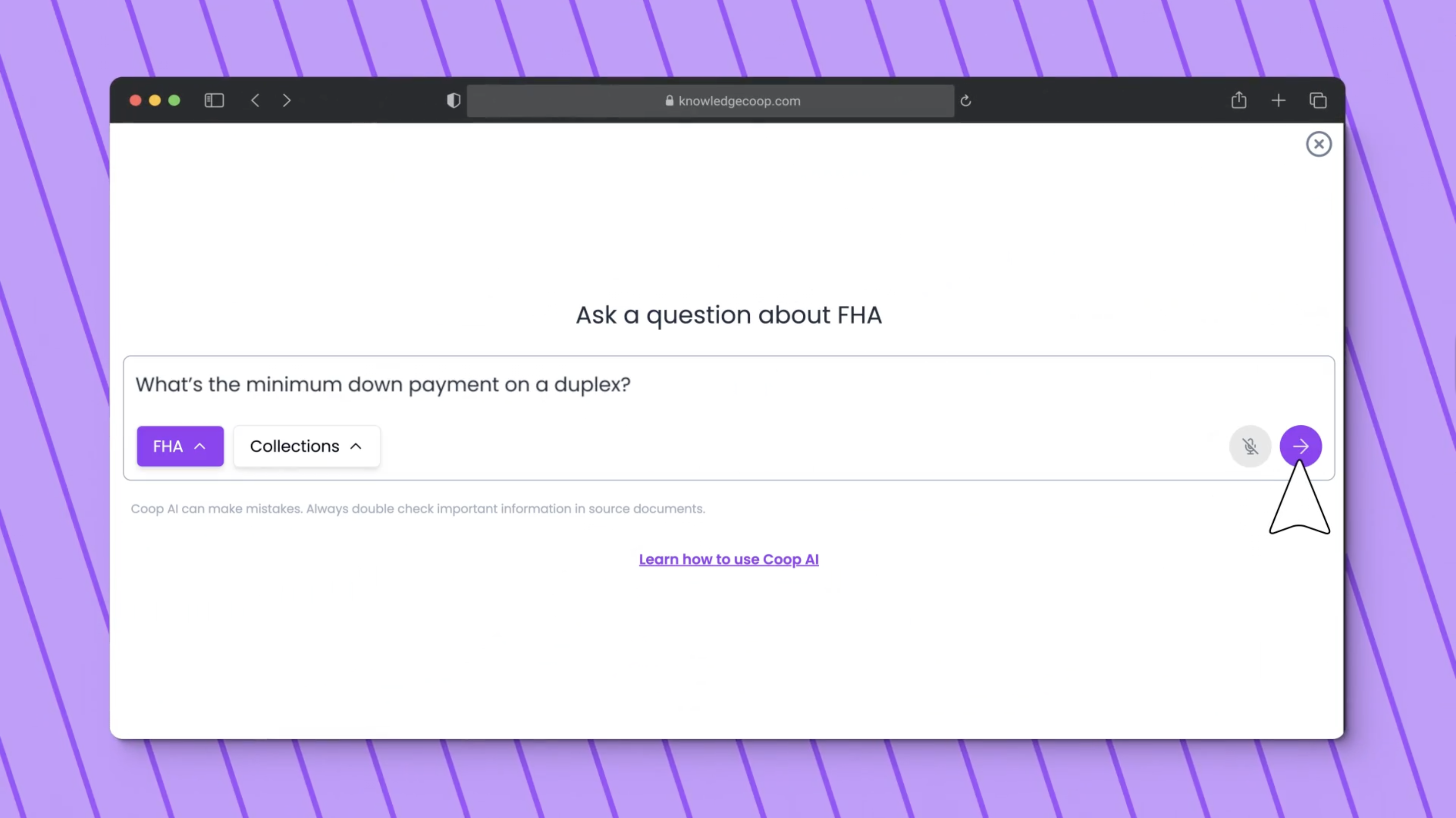

Custom Collections let teams centralize policies and get instant AI-powered answers.

Connect directly with industry experts and the minds behind our training. Subscribe to Coop+ for exclusive content, real-time insights, and interactive discussions that keep you ahead of the game.

.png)

.jpg)